By Kevin Lahey, CR and Dan Turpin | Published February 22, 2023

From devastating hurricanes to tornadoes, catastrophes (aka CATs) have impacted homes and businesses across the U.S. on a grand scale in the last few years. The result is the rising number of CAT claims.

For companies pricing out CAT projects, the labor shortage and supply chain continue to be a challenge. Now, add inflation and the rising cost to repair grows even larger. These have led to sticker shock at the time of repair estimates. Unfortunately, there is no immediate relief on the horizon.

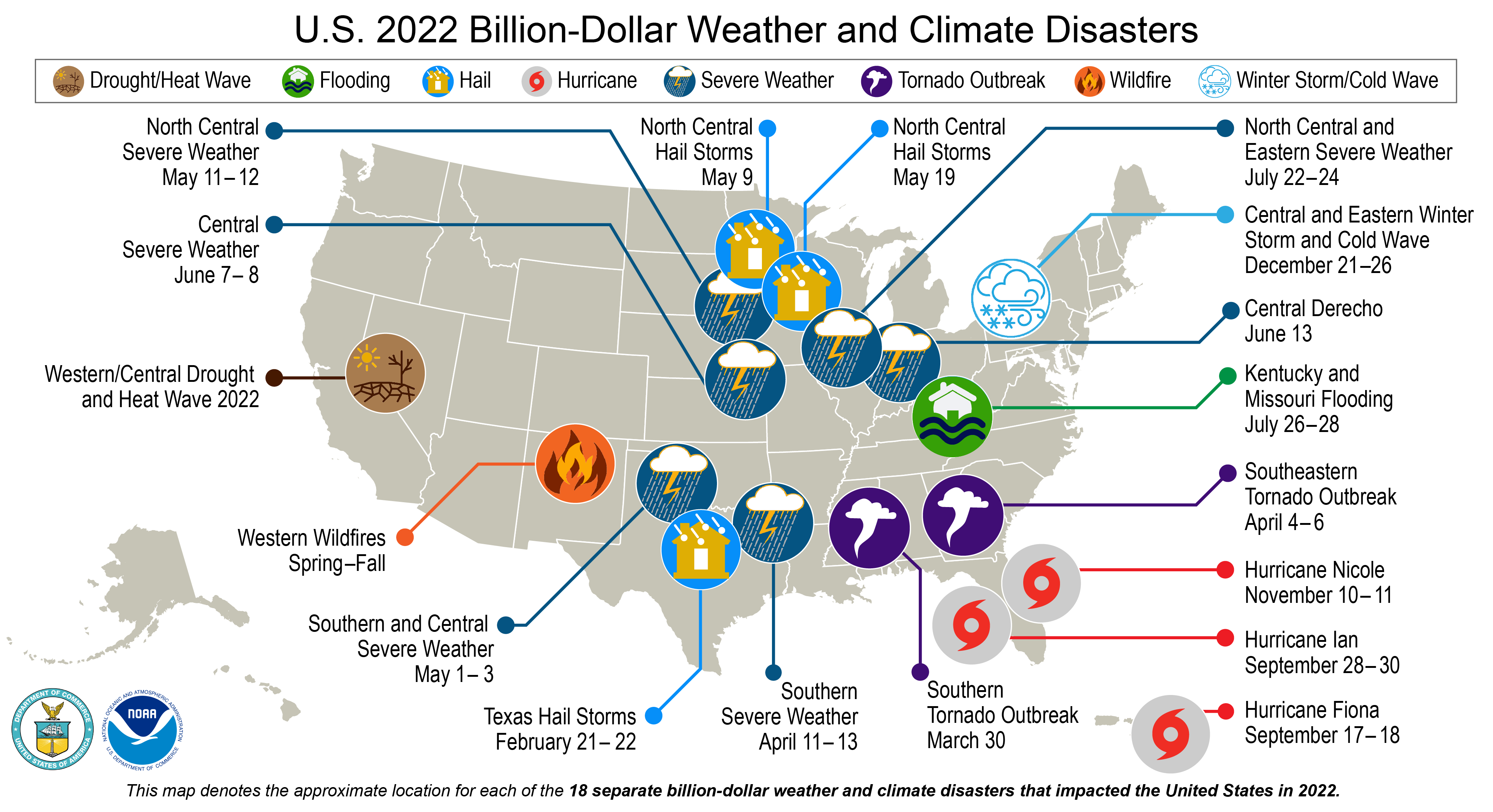

Natural disasters caused an estimated $115 billion in insured losses worldwide in 2022, with Hurricane Ian causing the most damage — an estimated $50 billion to $65 billon.1 Overall, U.S. disasters caused more than $165 billion in damages in 2022.2 The U.S. experienced 18 different weather and climate disasters in 2022, costing more than $1 billion each.3

3 Issues Affecting CAT Pricing

3 Issues Affecting CAT Pricing

The labor shortage and strained supply chain have had a noticeable impact on all construction pricing and timelines. Add the additional constraints of a regional catastrophe and things become even more expensive.

- Regional catastrophes are happening more frequently: In years past, it was more common for the U.S. to experience a singular CAT regional catastrophic event, or at least a long period between events. Today, regions have been devastated by back-to-back local events, making it harder to secure quality repair teams. The average price increase in a regional catastrophe situation is 27% above the region’s median construction cost, and this percentage goes up as more and more resources are exhausted due to multiple events in a particular region.

- Access issues: Hurricane-related rainfall is projected to increase 10% to 15% and intensity is projected to become 1% to 10% stronger later in the 21st century.4 The overall intensity of Atlantic hurricanes are projected to increase by 5% during the 21st century.4

While these projections are still in their infancy due to a lack of historical data, the evidence suggests a continued upward trend in rainfall and intensity, which has led to logistical nightmares accessing properties in a timely manner. Many severely impacted properties are not seen for up to 30 days due to flooding and infrastructure failures. Couple this with the additional strain on a dwindling labor force and you have a recipe for escalated damage cost due to the extended time structures set unmitigated and open to the elements.

- Lastly, we have seen the impact the period of restoration (aka POR) has had on pricing and repair. From supply chain issues to the shutdowns to lack of availability from architecture firms, the time to complete restoration projects has increased in general and during regional catastrophes, this only grows exponentially.

What Can Be Done?

It is more important than ever to combat the negative impacts of rising costs of CAT claims. A few things you can do immediately post-CAT claim:

- Place emphasis on the speed of the initial response. This sounds great in theory but a person can only do so much in a day. Lean on your experts to get out there to assess the building and help locate resources to speed up mitigation. If the owners have mitigation contracts in place already with a local vendor, this is a good time to use that leverage.

- Proactively order long lead item materials: Consider partial contracts with local general contractors to order long lead item materials until scope and price is agreed upon.

- Obtain an accurate scope of work: Lean on experts to identify the scope of work with the contractor of record (if possible). Having the agreed scope of work is crucial, especially in a CAT situation.

While the impact of today’s economic winds across the U.S. are significant, there are many ways we can work together to support clients and their need to rebuild quickly. Your partnering with the best experts is the key to lightening your load.

This information is intended for informational purposes only. Each restoration project has unique properties and must be evaluated individually by knowledgeable consultants. Additionally, cutting samples of roof assemblies should be performed by qualified professionals and in some instances approved by the roofing manufacturer. RMC Group is not liable for any loss or damage arising out of or in connection with the use of this information.

Sources:

1 Swiss Re Institute “Hurricane Ian drives natural catastrophe year-to-date insured losses to USD 115 billion, Swiss Re Institute estimates,” December 1, 2022.

2 National Centers for Environmental Information “Assessing the U.S. Climate in 2022,” January 10, 2023.

3 National Centers for Environmental Information “Billion-Dollar Weather and Climate Disasters,” January 10, 2023.

4 Geophysical Fluid Dynamics Laboratory “Global Warming and Hurricanes,” February 9, 2023.